|

#1

11-13-2007, 08:28 PM

11-13-2007, 08:28 PM

|

|||

|

|||

|

Katy PMed me and asked me to start a Lounge thread on the economy, specifically addressing things like:

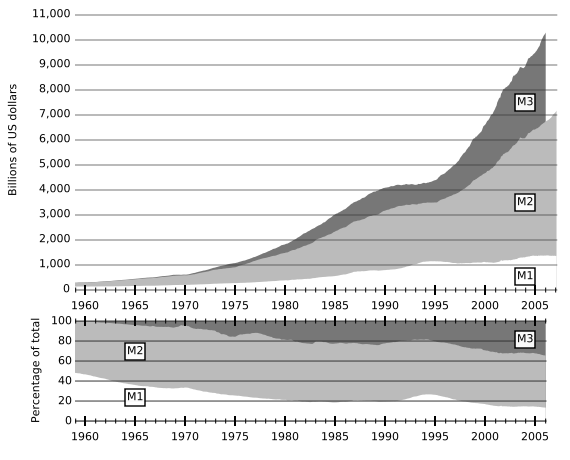

[ QUOTE ] . . . what's happening to our economy and what we can expect in the near future. For example, why is it bad for the feds to cut the interest rate? What is the meaning of "sub-prime" lenders and how is it that a few people defaulting on their loans could push the entire world into an economic crisis? [/ QUOTE ] While I am taking a stab at this, opinions are greatly varied and other people on the site disagree with my interpretations. They are certainly welcome to post their views as well. And I welcome all questions. Let's just please, please, please try to keep it Lounge-worthy, i.e. civil. I hate to have to ask this, but very often I've found that people with differing views on such things often cannot restrain themselves from hurling insults (myself included [img]/images/graemlins/tongue.gif[/img] ). Ok! Here's a little background, X-posted from a BFI post I just made, on how the Fed lowers interest rates by expanding the money supply, and what the negative effects of this are. It was in response to a question about some people (who generally subscribe to what's called the Austrian School of economics, like me) that claim that the Fed "prints money out of nothing": [ QUOTE ] When we say "printing money form nothing", it's a figure of speech. The money doesn't need to be physically printed to expand the money supply. An entry is simply created in an electronic account at the Fed, and then the Fed purchases government securities from special brokers during "Fed Time" in open market operations with that newly created money, via wire transfer I believe (although I'm not sure; the Fed might physically cut a check). Those brokers then deposit those funds in the commercial banks, where they become increased reserves for the banks. If commercial bank reserves are increased by $50B in this manner, the banks can then create up to a total of $500B via loans, by the magic of fractional reserve banking, if the reserve rate is 10% for example. The artificial lowering of the interest rate of course encourages people to take out these loans, which is what actually does most of the expansion of the money supply. <font color="white"> . </font> The important number is not the total of physical cash, but the total of fiduciary instruments, M3: <font color="white"> . </font>  <font color="white"> . </font> Before the Fed stopped reporting M3 (supposedly because it "cost too much" to measure; this from the people who can create money), M3 was expanding at about 15% per year. <font color="white"> . </font> And once again I will point out that artificially lowering the interest rate, which is really the market price for investment funds and hence access to physical resources, causes a misallocation of those physical resources, just as any price cap on any good or service causes a misallocation of that good or service. If you cap the price of milk at $0.25/gallon, people would be bathing in milk and watering their lawns with it, and a shortage would develop. That's what happens to the physical capital stock when the interest rate is artificially capped; productive capacity is misallocated and a shortage develops that is eventually revealed in, and correct by, a recession. [/ QUOTE ] Now, as for why the Fed does this, the going explanation is that without careful management of the money supply, the market economy is inherently subject to periodic instability, called business cycles, which are alternating "booms" and "busts". The claim is that a central bank must manage the money supply to navigate the economy through these, cooling off the booms and heating the economy back up in the busts. The Austrians would claim that it is bank credit inflation and the associated artificial lowering of the interest rate that causes the business cycle, of artificial booms and the busts required to correct them, in the first place. Austrians don't think that those within the Fed are stupid, however. After all, Alan Greenspan was an Austrian for decades before he took the reigns of the money supply. We are very cynical about why an institution like the Fed would want a monopoly of the power to legally create money out of nothing, and very cynical about the reasons for and timing of the artificially created booms. It is much easier to be re-elected for a second term as president if the Fed has turned on the money spigot, generating an artificial boom after the recession caused by your predecessor's re-election boom, and by the time your second term is up and your recession hits, it's the next administration's problem. If you look at the one sustained period of almost zero increase in the money supply in the graph above, it is the reign of George H. W. Bush, who still bitterly complains that Alan Greenspan cost him re-election. For a more extensive overview of the Austrian Business Cycle Theory (ABCT) see this post. On to the next question, which was about "sub-prime" lending. This is part and parcel of another general problem with credit expansion: asset bubbles. Expansion of the money supply eventually drives up prices, creating price inflation (the pattern and time structure of this inflation is complex, and I won't go into it; suffice it to say that not all prices go up equally or at the same time, and in fact some prices don't go up at all; they will fall). Investment funds, seeking to stay ahead of inflation, will tend to find their way into certain asset classes, which could be anything, stocks, real estate, art, etc. and create asset bubbles, or sectors of the economy that are particularly overvalued. The entire economy is actually bubbled because the lowered interest rate tends to trick entrepreneurs into making mistakes all across the economy, but some areas are always more bubbled than others. In any event, one of the latest bubbled sectors of the economy is housing, which the Austrians and others were pointing out as early as 2002 and 2003. The last big bubble we all heard about was the "dot com" bubble, i.e. technology stocks. So what is sub-prime lending? Well, when there is a market clearing interest rate, that means that everyone that wants to borrow at the market rate and everyone that wants to invest at the market clearing rate can always find someone to do business with. By lowering the interest rate, you trick buyers into entering the market who would not have entered the market at the real rate. "Sub-prime" lending basically refers to creating loans for buyers who would not have been able to get loans before, either because of credit problems, income, or whatever. Obviously the risk of default on these loans is higher than normal. The reason that this happened (and none of the people involved was stupid) was the asset bubble in real estate values. People saw real estate values rising so fast that buyers would be gaining equity so fast that the riskier loans appeared to be justified. The problem is that all bubbles must eventually burst. When the housing bubble started to burst, and real estate values began to fall, suddenly a lot of people are revealed to be WAY upside down in their mortgages. Now, even though foreclosures are up something like 400%, that's not the real issue. That is still a tiny fraction of homeowners being foreclosed on. The real problem is what was done with all of these mortgages. They were packed up and sold as securities, so-called Mortgage Backed Securities (MBS's). Now the MBS's became a VERY popular investment vehicle when the real estate market was hot. And there was then a secondary asset bubble in MBS's. A LOT of big financial institutions, foreign and domestic, invested a lot of money (hundreds of billions of dollars) into these securities. And now that the real estate bubble has popped, the underlying market value of these securities has also popped, and the banks have had to "write down" billions and billions in losses on these instruments. Accompanying all of this is the "credit crunch". People generally think the credit crunch is being driven by the sub-prime crisis, but it is more fundamental than that. The credit crunch is not tied to one sector, its economy wide, and it is a result of the earlier credit expansion. When the interest rate is lowered, it causes entrepreneurs all over the economy to believe that all sorts of new projects are profitable. Let's say the real interest rate is 8%. A project that returns 7% would be unprofitable to take out a loan with which to undertake it. But if the interest rate is artificially lowerd to 5%, that project looks profitable, and a business might take out that loan and start that project. The problem is that as entrepreneurs all over the economy are doing this, they start bidding up the prices of the inputs, the physical factors of production like steel, energy, computers, machines, equipment, labor, office and warehouse space, etc. There aren't enough physical factors of production to complete all these projects, and they eventually bid up the prices of the inputs to the point where the project is revealed to be unprofitable. The rising input prices cause an increase in the demand for loanable funds, which tries to drive up the interest rate, the "credit crunch". The Fed can either maintain the low interest rate by injecting more "liquidity", i.e. money, which it cannot do indefinitely, or it can let the interest rate rise, revealing all of these projects throughout the economy to be unprofitable malinvestments, which kicks off the recession. It is really not that the sup-prime mortgage crisis will "spill over" into the rest of the economy. The rest of the economy is also bubbled. It's just that one sector happened to be the first to pop, real estate. That dominoed into the MBS asset bubble. That dominoed into the financial institutions. Technology stocks are showing weakness, and I even saw that the art market took a massive hit. In 2000 it was dot coms and tech stocks that were the first to go, but they didn't drag the rest of the economy down with them; the rest of the economy was already poised to go. When 9/11 crashed the stock market, it didn't really do a trillion dollars of economic damage as I've heard people claim. That trillion dollars in economic damage had already been done by monetary inflation. It was just that the recession of 2000 and the acceleration of 9/11 revealed it. We have that same scale of economic damage now driven by the last 6 years of monetary inflation; it's just that it hasn't yet been fully revealed, and it probably won't be revealed quite so quickly. Lastly, I will talk about the dollar. For many years now the Fed has been expanding the money supply at a rapid pace. We have not seen very much of this in consumer prices for a couple of reasons. One, a large fraction of those new dollars go out of the country and end up being held by foreign central banks, mostly asian and middle eastern, as their reserves, on top of which they print their own fiat currencies. China alone holds something like US$1.5T. We have basically been exporting inflated dollars and importing real goods and services. This drives our massive trade deficit, and allows us to literally exploit the world (we get goods and services, they get green pieces of paper or electronic entries representing them). Another part of the monetary expansion is hidden in increasing productivity. If the money supply expands at 5% but productivity also rises at 5%, then prices will appear to be stable, even though monetary expansion and malinvestment is still occuring (this was the case in the 1920s). Now the problem is that by expanding the money supply, you obviously increase the supply of dollars. Since all the other countries are also expanding their money supplies, if the US expanded at the same rate as everyone else, there wouldn't be any general long term weakening in the dollar vs. other currencies like the Euro. But this isn't the case. The Fed has inflated the dollar supply at a faster rate than other currencies are being inflated, which lowers its international purchasing power relative to those currencies, weakening it relative to them. As the value of dollar holdings falls, people seek to get out of dollars, either by selling them on currency markets, which further increases their supply and lowers their demand, further lowering their value, or by buying up assets for US dollars, which drives up asset prices. As the value of the dollar falls internationally, the best place to buy assets like real estate and companies for US dollars will be the US. So foreign investment will go up, our exports are going up, but all those inflated dollars coming home to roost will drive up domestic prices. So what we are set for is staglation; we are entering a recession at the same time we will see significant price inflation. The last time this happened was the 1970s, and that occured for largely the same reasons it is happening now. This turned out to be a much longer post than I thought. Keep in mind that others will greatly disagree with my interpretation, and I don't claim that my understanding of abstruse investment instruments like mortgage backed securities is perfect. I welcome thoughts, corrections, questions, and other contributions.

|

|

#2

11-13-2007, 09:05 PM

|

|||

|

|||

|

[ QUOTE ]

When we say "printing money form nothing", it's a figure of speech. The money doesn't need to be physically printed to expand the money supply. An entry is simply created in an electronic account at the Fed, and then the Fed purchases government securities from special brokers during "Fed Time" in open market operations with that newly created money, via wire transfer I believe (although I'm not sure; the Fed might physically cut a check). Those brokers then deposit those funds in the commercial banks, where they become increased reserves for the banks. If commercial bank reserves are increased by $50B in this manner, the banks can then create up to a total of $500B via loans, by the magic of fractional reserve banking, if the reserve rate is 10% for example. The artificial lowering of the interest rate of course encourages people to take out these loans, which is what actually does most of the expansion of the money supply. [/ QUOTE ] Thanks for addressing all my questions to you Borodog. I really appreciate the time you put into your OP! Awesome. A lot of this stuff is a little over my head but I want to see if I understand some of the basic concepts. Forgive me if I screw this up but what the hell, here goes. Lowering interest rates by increasing reserves Are you saying that when the Fed lowers interest rates it first creates paperless funds (in other words expands the money supply) for commercial banks so that they can make more loans to people. So making more loans to people is the big goal right? Is this the first step in lowering the interest rate or did I misunderstand you? Sorry I'm sounding so ignorant, I just did not realize that the term "lowering the interest rate" meant creating more funds for banks to loan out. And why would banks want to make all these loans if people are in such a shaky position with high mortgages and credit card problems? I would guess they don't want to loan to private citizens as much as they do to businesses and corporations. Gah, economics and I are complete strangers [img]/images/graemlins/grin.gif[/img]

|

|

#3

11-13-2007, 09:44 PM

|

|||

|

|||

|

Borodog. I am very interested in this subject.

Did you know that Greenspan was a student of Ayn Rand? I am also under the impression that credit is weakening the dollar. I calculated that the dollar is only about 1/10th of it's actual value because there is way more credit than actual money. Am I correct in my assertion. How do you think this is effecting the dollar, and is this why the interest rates change?

|

|

#4

11-13-2007, 09:53 PM

|

|||

|

|||

|

Great post. I have several questions:

1. The newly printed dollar is actually worth less than a dollar. Please explain why. 2. A year or two ago I watched an interview on Charlie Rose with an economist who was articulating concerns about the trade deficit. Your thoughts? 3. I work in commercial construction in FL. The burst housing bubble effects have been acute and pronounced. With the weakened dollar, I am actually optimistic because of the predicted influx of foreign investment on the local level. Am I wrong?

|

|

#5

11-13-2007, 09:54 PM

|

|||

|

|||

|

haven't read the entire op yet, but this is a great idea. hopefully this goes better than policy talk in politics

|

|

#6

11-13-2007, 09:56 PM

|

|||

|

|||

|

[ QUOTE ]

So what is sub-prime lending? Well, when there is a market clearing interest rate, that means that everyone that wants to borrow at the market rate and everyone that wants to invest at the market clearing rate can always find someone to do business with. By lowering the interest rate, you trick buyers into entering the market who would not have entered the market at the real rate. "Sub-prime" lending basically refers to creating loans for buyers who would not have been able to get loans before, either because of credit problems, income, or whatever. [/ QUOTE ] [ QUOTE ] Now, even though foreclosures are up something like 400%, that's not the real issue. That is still a tiny fraction of homeowners being foreclosed on. The real problem is what was done with all of these mortgages. They were packed up and sold as securities, so-called Mortgage Backed Securities (MBS's). Now the MBS's became a VERY popular investment vehicle when the real estate market was hot. And there was then a secondary asset bubble in MBS's. A LOT of big financial institutions, foreign and domestic, invested a lot of money (hundreds of billions of dollars) into these securities. [/ QUOTE ] Ok some of this is actually starting to make sense to me. I was hearing how the foreclosures had caused a world wide banking crisis and I kept wondering how in the heck a few American slackers who couldn't handle their mortgages and credit cards could be responsible for throwing world banks into crisis. It just made no sense to me. Someone on one of the forums said that the housing bust in America was messing with the European economy and I was like huh? You've got to be kidding! But now that you explain that the major banks had invested in the MSB's I can sort of see this domino effect. 1. Have there always been sub-prime lenders or is this a relatively new phenomenon? 2. You say that these risky loans looked justifiable...but to whom? The sub-prime lender, the MBS's, or the customer? Did the sub-prime companies know this would happen and is this why they turned around and sold the mortgages quickly? 3. What kind of financial institution would think this was a good idea? It seems like this kind of outcome could be predicted. Overall, what company suffered the most from the housing bubble bust? The large banks? 4. I wonder if any of my mutual funds were invested in these MSB's.

|

|

#7

11-13-2007, 10:16 PM

|

|||

|

|||

|

Wheee economics by borodog! Last time I participated in one of these I learned a lot about Austrian economics, I hope this one becomes just as interesting.

[ QUOTE ] 1. Have there always been sub-prime lenders or is this a relatively new phenomenon? [/ QUOTE ] Sub-prime borrowers are just a class of borrowers who have a higher credit risk. What's recent (prior to subprime meltdown) is the amount of subprime lending done without tight standards and the increasing ways in which this debt is held, in the form of structured products. The widespread investment in this risky debt and errors in risk management is what led to problems. [ QUOTE ] 2. You say that these risky loans looked justifiable...but to whom? The sub-prime lender, the MBS's, or the customer? Did the sub-prime companies know this would happen and is this why they turned around and sold the mortgages quickly? [/ QUOTE ] The loans looked justifiable to everyone, that's why there was a market for these things. Not sure what you're getting at here. Some (like Warren Buffett) predicted that this would happen with all the non transparency but there was such a strong potential for profiting off the interest from the subprime mortgages that a lot of people jumped in anyway. [ QUOTE ] 3. What kind of financial institution would think this was a good idea? It seems like this kind of outcome could be predicted. Overall, what company suffered the most from the housing bubble bust? The large banks? [/ QUOTE ] Any financial services firm or institution trying to make money would have been interested in this. The housing bubble supported the stream of payments from these babies, and there was a lot of money being made off these. One of my professors invented the method of tranching mortgages into different levels of risk and he's now ridiculously wealthy. Any type of company exposed to housing, consumer spending, or the debt instruments themselves suffered from the housing bubble bursting. [ QUOTE ] 4. I wonder if any of my mutual funds were invested in these MSB's. [/ QUOTE ] Probably not directly but they all probably had some level of exposure in the form of stock of banks, construction companies, etc.

|

|

#8

11-13-2007, 10:21 PM

|

|||

|

|||

|

wrt lowering of interest rates through credit expansion, you can read this katy:

http://en.wikipedia.org/wiki/Money_supply

|

|

#9

11-13-2007, 10:31 PM

|

|||

|

|||

|

[ QUOTE ]

So what we are set for is staglation; we are entering a recession at the same time we will see significant price inflation. The last time this happened was the 1970s, and that occured for largely the same reasons it is happening now. [/ QUOTE ] Borodog can you expand on this? As far as I am aware, oil prices are leading to inflation but growth is still rather strong. I checked the latest economic data from the Fed and there was 3.9% growth in the last quarter, and very little spillover from housing into other sectors. But I'm writing a paper right now and cannot do further research [img]/images/graemlins/frown.gif[/img]

|

|

#10

11-13-2007, 11:12 PM

|

|||

|

|||

|

[ QUOTE ]

Lowering interest rates by increasing reserves Are you saying that when the Fed lowers interest rates it first creates paperless funds (in other words expands the money supply) for commercial banks so that they can make more loans to people. So making more loans to people is the big goal right? Is this the first step in lowering the interest rate or did I misunderstand you? Sorry I'm sounding so ignorant, I just did not realize that the term "lowering the interest rate" meant creating more funds for banks to loan out. [/ QUOTE ] The real intention of the Fed when it lowers the interest rate is to "stimulate the economy." In other words, it wants more transactions taking place in the economy. It does this by lowering interest rates, which encourage businesses and individuals to take out loans with the intention of buying stuff with the money. The reason that lowering the interest rate encourages people to take out a loan is that the interest rate is essentially the price of money over a certain time horizon. If I asked you to loan me $10,000 for a year, and promised to give you exactly $10,000 after one year, you would laugh at me (unless there were special circumstances like we were good friends, etc.). I would have to pay you a price, say promise to give you $11,000 after one year for your $10,000 now. That would be a 10% interest rate. So the market interest rate is the rate set by the supply of loanable funds (i.e. money saved up and not spent by people on consumption) and the demand for loans. The higher the supply of loanable funds, the lower the price of money (the interest rate). The lower the supply, the higher the interest rate. So by creating more money to be loaned out, the Fed increases the supply of loanable funds, which lowers the interest rate, which encourages people to take out loans, because it coasts them less to do so, which encourages spending in the economy. The problem is that this whole process, while it appears great (a boom) it is actually very damaging to the structure of the economy. Make sense? [ QUOTE ] And why would banks want to make all these loans if people are in such a shaky position with high mortgages and credit card problems? I would guess they don't want to loan to private citizens as much as they do to businesses and corporations. Gah, economics and I are complete strangers [img]/images/graemlins/grin.gif[/img] [/ QUOTE ] The banks want to make loans because they make interest off of them. Now they will obviously be willing to make shakier loans if they are making interest off of money that was created from nothing than if the principle they are risking was not created from nothing. They still want to make loans to the best risks possible, but hey, when the good risks are all serviced and you still want to make loans and earn interest, you will start making shakier and shakier loans. Also, it wasn't just banks that were making sub-prime mortgages. There were a lot of mortgage brokers looking to cash in on the mortgage bonanza created by the housing boom. A lot of funding for these mortgages came from real savings, i.e. investors, rather than being printed from nothing. But since they must compete with the banks for loans, when the banks depress the interest rates, they do so market wide. Those investors turned around and sold those mortgages to be packaged as mortgage backed securities. The brokers and their investors were making money hand over fist; it was the people who bought the MBSs that were eventually left holding the bag. And remember, at the time that all of these shaky mortgages were being put together, all the participants thought that the market warranted it because of skyrocketting real estate values. It was only after the housing bubble popped that the problem was revealed, which is the nature of a recession across the entire economy.

|

|

|

|

Linear Mode

Linear Mode